All Categories

Featured

Table of Contents

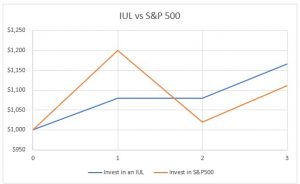

Below is a hypothetical comparison of historical efficiency of 401(K)/ S&P 500 and IUL. Allow's think Mr. SP and Mr. IUL both had $100,000 to saved at the end of 1997. Mr. SP invested his 401(K) cash in S&P 500 index funds, while Mr. IUL's cash was the cash money worth in his IUL policy.

IUL's plan is 0 and the cap is 12%. After 15 years, at the end of the 2012, Mr. SP's profile grew to. Due to the fact that Mr. IUL never shed cash in the bear market, he would have twice as much in his account Even much better for Mr. IUL. Considering that his money was saved in a life insurance policy policy, he doesn't require to pay tax! Certainly, life insurance protects the family members and offers sanctuary, foods, tuition and clinical expenses when the insured dies or is seriously ill.

Iul Mutual Of Omaha

Life insurance policy pays a fatality benefit to your beneficiaries if you ought to die while the plan is in impact. If your household would deal with financial challenge in the occasion of your fatality, life insurance offers tranquility of mind.

It's not one of the most profitable life insurance policy investment strategies, however it is among the most safe. A type of irreversible life insurance policy, universal life insurance allows you to pick exactly how much of your costs goes towards your survivor benefit and just how much enters into the policy to gather money worth.

Additionally, IULs allow insurance holders to obtain financings versus their policy's cash money value without being strained as earnings, though unsettled balances may undergo taxes and penalties. The main advantage of an IUL policy is its capacity for tax-deferred development. This means that any type of profits within the plan are not tired till they are taken out.

Alternatively, an IUL policy might not be the most ideal savings plan for some people, and a standard 401(k) could show to be more helpful. Indexed Universal Life Insurance Policy (IUL) policies use tax-deferred growth potential, defense from market downturns, and survivor benefit for recipients. They permit insurance holders to make rate of interest based upon the performance of a stock exchange index while securing against losses.

Iul Illustration

A 401(k) strategy is a prominent retirement cost savings alternative that allows individuals to invest money pre-tax right into various financial investment devices such as mutual funds or ETFs. Companies may likewise use matching payments, even more boosting your retired life savings possibility. There are two major kinds of 401(k)s: traditional and Roth. With a standard 401(k), you can lower your taxable income for the year by contributing pre-tax bucks from your income, while likewise taking advantage of tax-deferred growth and company matching payments.

Several companies also give coordinating contributions, properly giving you cost-free cash towards your retirement plan. Roth 401(k)s feature similarly to their conventional equivalents however with one secret distinction: taxes on payments are paid ahead of time as opposed to upon withdrawal throughout retired life years (The Differences Between Roth IRA and IUL: What You Need to Know). This suggests that if you anticipate to be in a higher tax obligation brace throughout retired life, contributing to a Roth account could save money on taxes with time contrasted with investing entirely through traditional accounts (resource)

With lower management fees generally contrasted to IULs, these kinds of accounts allow capitalists to save money over the long-term while still benefiting from tax-deferred development potential. Additionally, many popular low-cost index funds are offered within these account types. Taking distributions prior to getting to age 59 from either an IUL plan's cash value by means of finances or withdrawals from a conventional 401(k) plan can result in adverse tax obligation implications if not dealt with meticulously: While obtaining versus your plan's money value is usually taken into consideration tax-free as much as the amount paid in costs, any kind of overdue lending balance at the time of fatality or policy surrender might go through earnings tax obligations and penalties.

Iul Instruments Gmbh

A 401(k) provides pre-tax investments, company matching contributions, and potentially even more financial investment options. The disadvantages of an IUL include greater management prices contrasted to standard retired life accounts, restrictions in investment options due to plan restrictions, and prospective caps on returns throughout strong market performances.

While IUL insurance coverage might show useful to some, it is very important to comprehend just how it functions prior to buying a plan. There are numerous advantages and disadvantages in comparison to various other forms of life insurance policy. Indexed global life (IUL) insurance coverage supply higher upside possible, adaptability, and tax-free gains. This sort of life insurance policy offers permanent insurance coverage as long as premiums are paid.

As the index relocates up or down, so does the rate of return on the cash value component of your policy. The insurance coverage business that releases the policy may supply a minimal guaranteed rate of return.

Financial experts frequently encourage living insurance policy protection that's equal to 10 to 15 times your yearly income. There are numerous drawbacks connected with IUL insurance coverage policies that doubters fast to explain. Somebody that develops the plan over a time when the market is carrying out poorly could finish up with high premium payments that don't add at all to the money value.

In addition to that, remember the complying with various other factors to consider: Insurance coverage business can establish participation prices for exactly how much of the index return you receive annually. For instance, let's claim the plan has a 70% participation rate (dave ramsey on iul). If the index grows by 10%, your cash worth return would certainly be only 7% (10% x 70%)

Furthermore, returns on equity indexes are usually capped at a maximum quantity. A policy could state your maximum return is 10% annually, no matter just how well the index does. These limitations can limit the actual price of return that's attributed toward your account each year, no matter how well the plan's underlying index carries out.

Aviva Iul

IUL plans, on the various other hand, offer returns based on an index and have variable premiums over time.

There are several various other sorts of life insurance policy policies, explained listed below. provides a fixed advantage if the insurance holder dies within a set amount of time, generally in between 10 and three decades. This is just one of the most budget friendly sorts of life insurance policy, in addition to the easiest, though there's no money value build-up.

Iul 保险

The plan gets value according to a dealt with timetable, and there are fewer charges than an IUL policy. A variable policy's cash value may depend on the performance of particular stocks or other safeties, and your costs can also alter.

{kind=link}

Table of Contents

Latest Posts

Iul Vs Whole Life

Www Iul

Best Indexed Universal Life Insurance Policies

More

Latest Posts

Iul Vs Whole Life

Www Iul

Best Indexed Universal Life Insurance Policies